Why ESGTree? – Differences that Make a Difference

Differences that Make a Difference: What distinguishes ESGTree from its competitors. Over the past four years, one of the most common questions we get is: What differentiates ESGTree from

Compliance Under the Australian Sustainability Reporting Standards (ASRS)

On 17 September 2024, the Treasury Laws Amendment (Financial Market Infrastructure and Other Measures) Act 2024 received Royal Assent, amending the Corporations Act 2001 to mandate climate-related financial disclosures for large Australian businesses and financial institutions. From financial years beginning on or after 1 January 2025, this framework is law.

The question is no longer whether your organisation should prepare for sustainability reporting. The question is what happens if you do not.

False or misleading climate statements can result in civil penalties of up to $15 million or 10% of annual turnover, whichever is greater. Directors may be held personally liable. Criminal offences carry a maximum prison penalty of 15 years.

These are not hypothetical consequences. They are embedded in the existing liability framework of the Corporations Act and the Australian Securities and Investments Commission Act 2001, and they apply to sustainability reports with the same force they apply to financial reports. As ASIC Commissioner Kate O’Rourke stated in September 2024, businesses should proactively engage with these mandatory climate reporting requirements and implement appropriate governance arrangements ahead of the obligations taking effect.

Sources: ASIC Media Release 24-205MR, September 2024 ; Treasury Laws Amendment Act 2024 ; Thomson Geer–Australia’s Landmark Climate Reporting Regime

This thought leadership piece is designed to provide directors, executives, and governance professionals with a clear understanding of what Australia’s mandatory climate reporting regime requires, the personal obligations it creates, and why early action is not merely advisable but essential.

AASB S2 Climate-related Disclosures, issued by the Australian Accounting Standards Board in September 2024, is the mandatory standard at the heart of this regime. It is closely aligned with IFRS S2, the global benchmark issued by the International Sustainability Standards Board, and it is built on the same four-pillar structure originally developed by the Task Force on Climate-related Financial Disclosures (TCFD).

These four pillars are not suggestions. They are the legally mandated structure for climate-related reporting under the Corporations Act.

Sources: AASB S2 Climate-related Disclosures (AASB Digital Standards Portal) ; AASB Standards Announcement

Organisations must disclose the governance processes, controls, and procedures they use to monitor, manage, and oversee climate-related risks and opportunities. This includes how the board and management are structured to address these issues, whether specific roles or committees have been assigned responsibility, and how climate considerations feed into strategic decision-making. This pillar is about demonstrating that climate risk oversight is not delegated to a sustainability team working in isolation. It must be embedded at the board and executive level, with clear lines of accountability.

Organisations must disclose how climate-related risks and opportunities have affected or are anticipated to affect their business model, strategy, and financial performance. This includes current and anticipated financial effects, as well as the entity’s Climate Transition Plan.

A particularly demanding requirement under AASB S2 is the mandatory climate scenario analysis. Unlike IFRS S2, which does not prescribe specific scenarios, the Australian standard requires entities to model at least two scenarios: one consistent with 1.5°C global warming, and another “high warming” scenario that significantly exceeds 2°C. This analysis is intended to test the resilience of an entity’s strategy under materially different climate futures.

Sources: AASB S2 Climate-related Disclosures, Appendix B ; Watershed–Australian Sustainability Reporting Standard

This pillar requires disclosure of the processes used to identify, assess, prioritise, and monitor climate-related risks and opportunities, and how those processes integrate into the entity’s broader risk management framework. The intent is to demonstrate that climate risk is managed alongside and within the same structures as operational, financial, and strategic risk.

Entities must disclose quantitative and qualitative climate-related metrics and targets. From Year 1, this includes Scope 1 and Scope 2 greenhouse gas emissions, calculated on a location basis. From Year 2, material Scope 3 emissions, including those across the value chain and, for financial institutions, financed emissions, must also be reported. This is where the reporting becomes most data-intensive. Organisations need robust systems to capture, verify, and present emissions data that will withstand assurance scrutiny.

Sources: AASB S2 Climate-related Disclosures ; ASIC Regulatory Guide 280, March 2025

Under the amended Corporations Act, the sustainability report must include a directors’ declaration confirming that the climate statements and accompanying notes comply with the Act and AASB S2. This declaration must be made in accordance with a board resolution, must specify the date, and must be signed by a director.

For financial years commencing between 1 January 2025 and 31 December 2027, directors must declare whether, in their opinion, the entity has taken reasonable steps to ensure the substantive provisions of the sustainability report comply with the Corporations Act. After this transitional period, the full standard declaration requirements will apply.

This is personal. While directors may rely on the special knowledge of their staff or external consultants, ASIC’s Regulatory Guide 280 makes clear that directors must still exercise independent care and diligence. They must understand the climate-related financial risks and opportunities that materially affect their business and ensure that appropriate systems, internal controls, and oversight mechanisms are in place.

Put simply, a director cannot claim ignorance. The existing duties under the Corporations Act, including the duty to act with care and diligence, now explicitly encompass sustainability reporting. As legal commentary has noted, directors who are not across this space risk personal liability, reputational damage, and shareholder scrutiny.

Sources: ASIC Regulatory Guide 280 (RG 280.57 – 60) ; Hamilton Locke – ASIC RG 280 in Practice

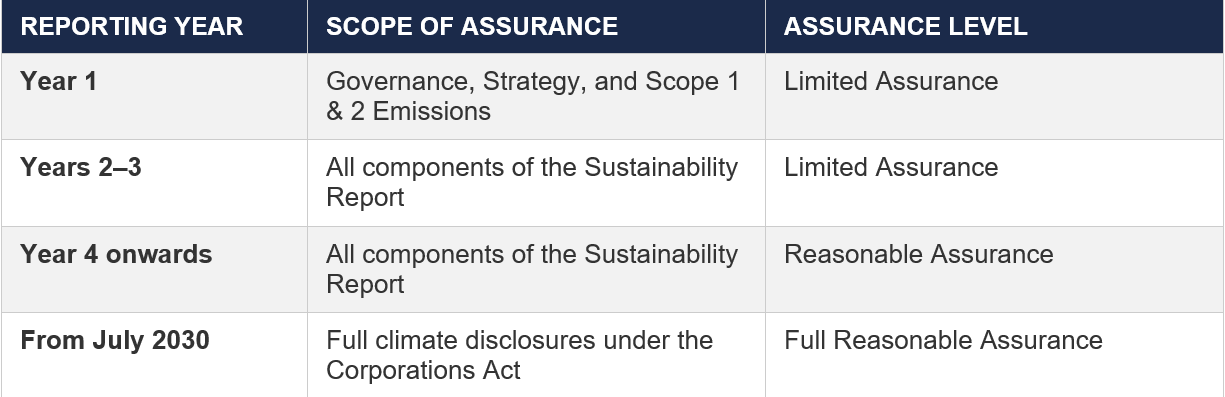

One of the most significant features of this regime is that assurance requirements begin from the very first year of mandatory reporting. There is no grace period in which organisations can submit disclosures without independent scrutiny.

In January 2025, the Australian Auditing and Assurance Standards Board approved ASSA 5000 (General Requirements for Sustainability Assurance Engagements) and ASSA 5010 (the timeline for phasing in assurance requirements). Together, these standards establish a structured pathway from limited assurance to full reasonable assurance.

Sources: AUASB ASSA 5000 & ASSA 5010, January 2025 ; PwC Australia–Sustainability Reporting Standards Finalised ; KPMG Australia–Australian Sustainability Reporting Standards Finalised

This means that even in the first year, organisations must have their governance disclosures, strategy disclosures, and Scope 1 and 2 emissions data at a level of rigour that can withstand independent review. An organisation cannot simply say anything and expect it to go unchallenged.

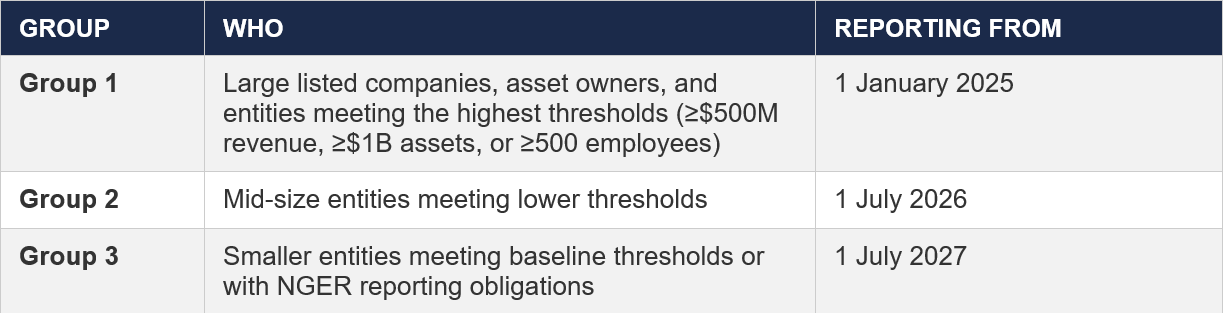

The regime applies to entities with financial reporting obligations under Chapter 2M of the Corporations Act that meet specific size thresholds or have emissions reporting obligations under the National Greenhouse and Energy Reporting (NGER) scheme. Implementation is phased across three groups:

Critically, Australian subsidiaries of international parent companies (ASIC) cannot rely on an overseas parent’s consolidated sustainability report to satisfy Australian requirements. Each in-scope subsidiary must prepare its own report, approved by its Australian directors, and lodged with ASIC.

Sources: Australian Government, The Treasury, Climate-related financial reporting and guidance (Treasury, 2026) ; Corporations Act 2001, s292A ; ASIC RG 280.35–42 ; DLA Piper–Key Elements of Australia’s Mandatory Climate Reporting

The regime does include a transitional modified liability framework to encourage complete disclosure during the early years. For financial years between 1 January 2025 and 31 December 2027, certain “protected statements” in the sustainability report are shielded from civil action, except by ASIC or in criminal proceedings.

Protected statements include Scope 3 emissions disclosures, scenario analysis, and transition plans for the first three years, and other forward – looking statements for the first 12 months. However, this protection is extremely limited in scope:

The modified liability settings should not be mistaken for blanket immunity. They are a carefully scoped transitional measure, and organisations that treat them as a reason to delay rigorous preparation will find themselves exposed when the full liability framework takes effect.

Sources: Corporations Act 2001, Division 3A ; ASIC RG 280.61–65 ; K&L Gates–Mandatory Climate-Related Financial Disclosures ; Clayton Utz–New ASIC Guidance on Sustainability Reporting

The introduction of mandatory sustainability reporting under AASB S2 is not an incremental regulatory adjustment. It is, as multiple legal and professional commentators have described it, a generational shift in corporate transparency. Climate-related risk has been legally elevated to the same status as traditional financial risk, subject to the same oversight, legal duties, and enforcement mechanisms. For directors, this means personal accountability. For boards, this means governance transformation. For organisations, this means investment in systems, data, expertise, and assurance-readiness from the very first reporting period.

Conduct a gap analysis against AASB S2 requirements. Embed climate risk oversight into board-level governance structures. Establish robust data systems for Scope 1, 2, and 3 emissions capture and verification. Engage assurance providers early. Ensure directors are fully briefed on their declaration obligations. Treat sustainability reporting with the same rigour as financial reporting.

The Australian Government’s Treasury Policy Statement on this regime was clear: a rigorous, internationally aligned and credible climate disclosure regime will support Australia’s reputation as an attractive destination for international capital and help draw the investment required for the transition to net zero.

The organisations that act now will not only meet their legal obligations. They will build the trust, transparency, and strategic resilience that investors, regulators, and stakeholders increasingly demand.

Sources: Australian Government, The Treasury, Climate-related financial reporting and guidance (Treasury, 2026) ; AICD–Boardroom Readiness for AASB S2 Climate Disclosures

For those seeking a streamlined approach, ESGTree’s advanced carbon calculator can handle all calculations for both your institution and your portfolio. Reach out to us to learn more!

Canada: ESGTree, CPA 4th Floor, 140 West mount Rd N, Waterloo,

ON N2L 3G6, Canada

United Kingdom: ESGTree, 33 Queen Street, London EC4R 1AP, United Kingdom