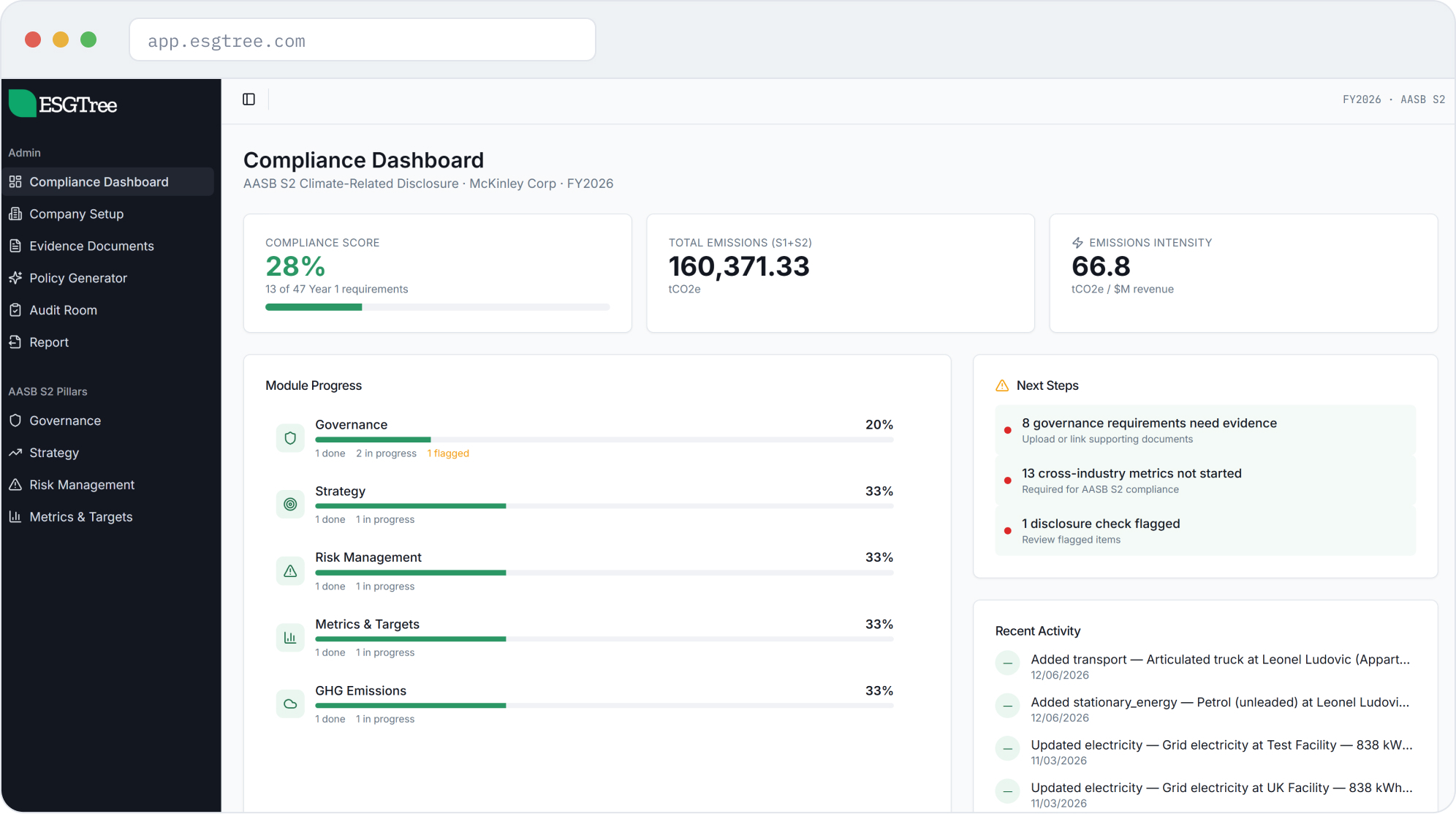

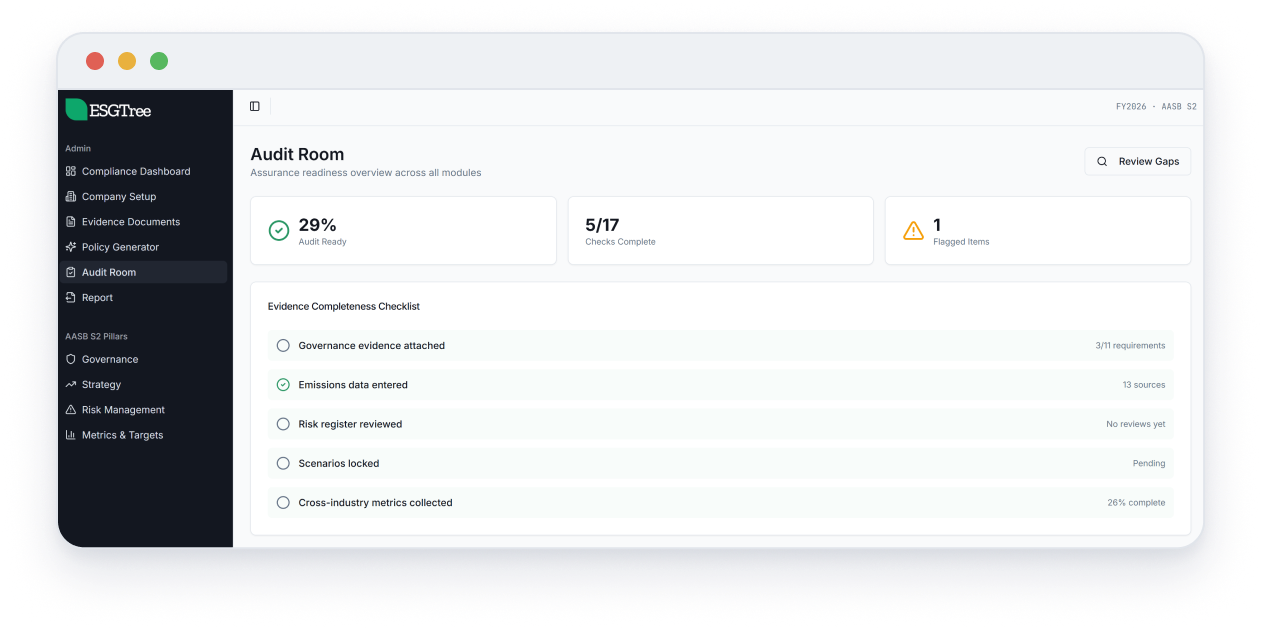

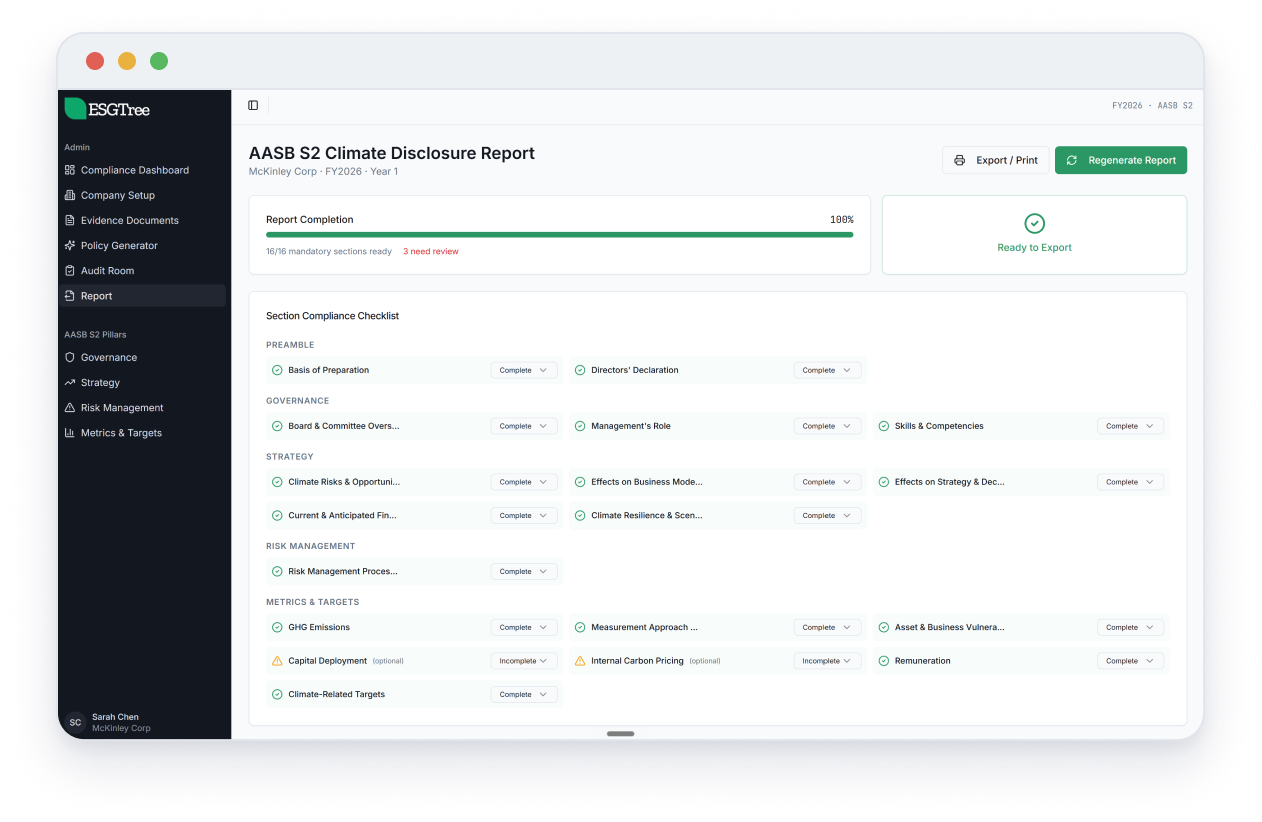

Governance

Board and management oversight of climate-related risks and opportunities. How responsibilities are assigned, how information flows to decision-makers, and how climate considerations are embedded in strategic oversight.

Strategy

How climate-related risks and opportunities affect your business model, financial position, and prospects over the short, medium, and long term. Includes climate scenario analysis and your transition plan.

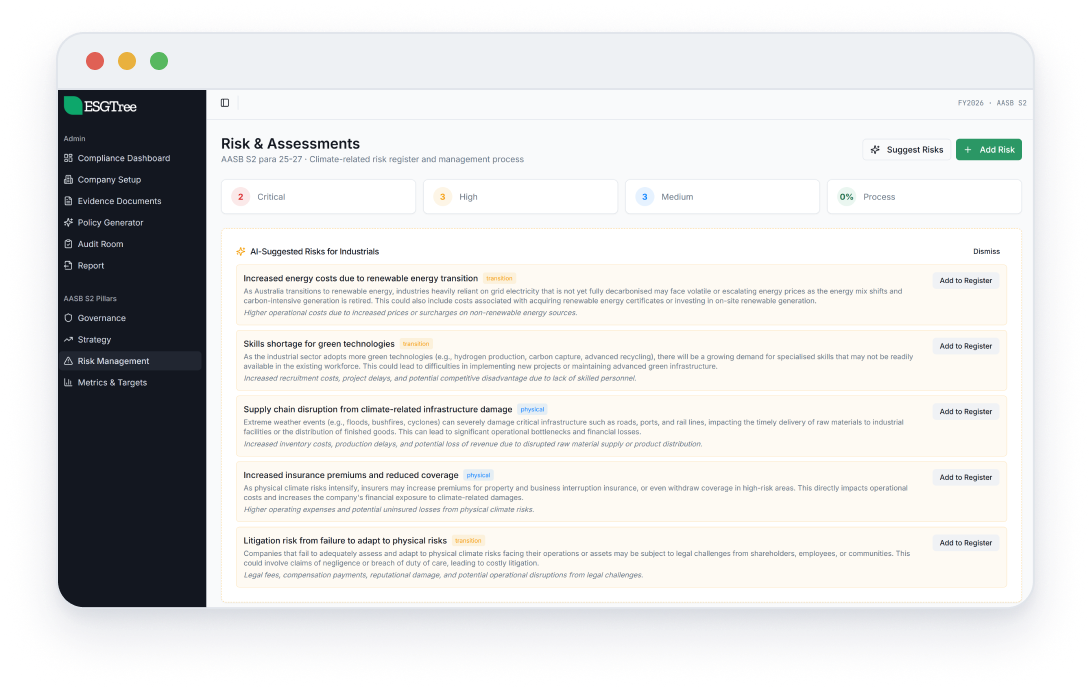

Risk Management

How you identify, assess, prioritise, and monitor climate-related risks, and how those processes integrate with your broader enterprise risk framework.

Metrics & Targets

Your Scope 1, 2, and 3 greenhouse gas emissions, calculated in accordance with the GHG Protocol. Plus any climate-related targets and your progress against them.

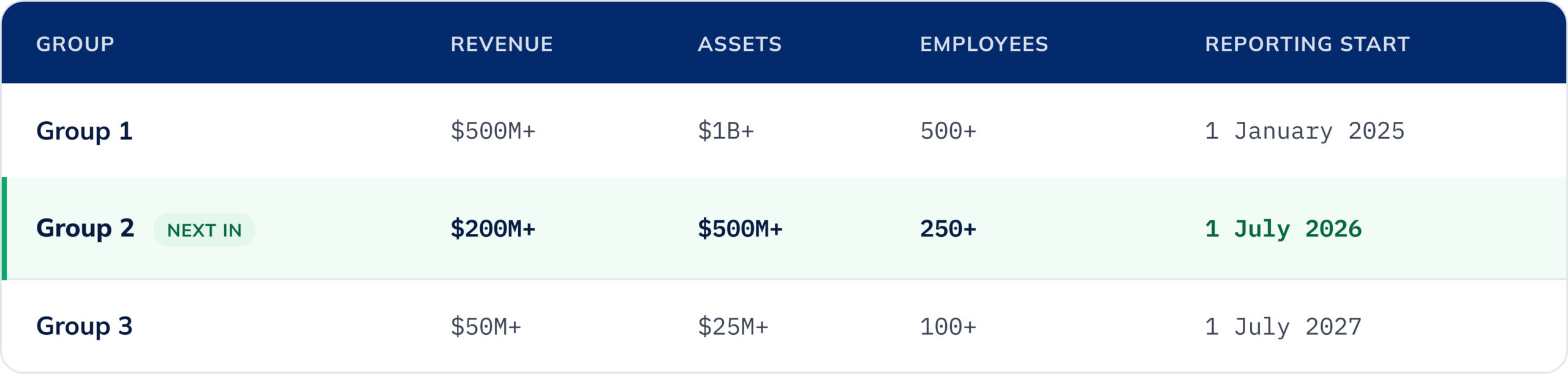

Asset owners with $5B+ AUM

Superannuation funds, registered schemes, and retail CCIVs are captured under Group 2, regardless of the revenue and employee tests.

1 July is the start, not the deadline

It marks when collection, calculation, and governance must be operational. The report is due to ASIC within four months of your year end.

Heavy reliance on transitional relief

Deferrals used to fill gaps that will come due in year two.

Limited Scope 3 disclosure

Value chain emissions left largely unreported.

Variable scenario analysis

Wide gaps in rigour and depth between reporters.

No traceable evidence trail

Governance claims assurance teams could not verify.

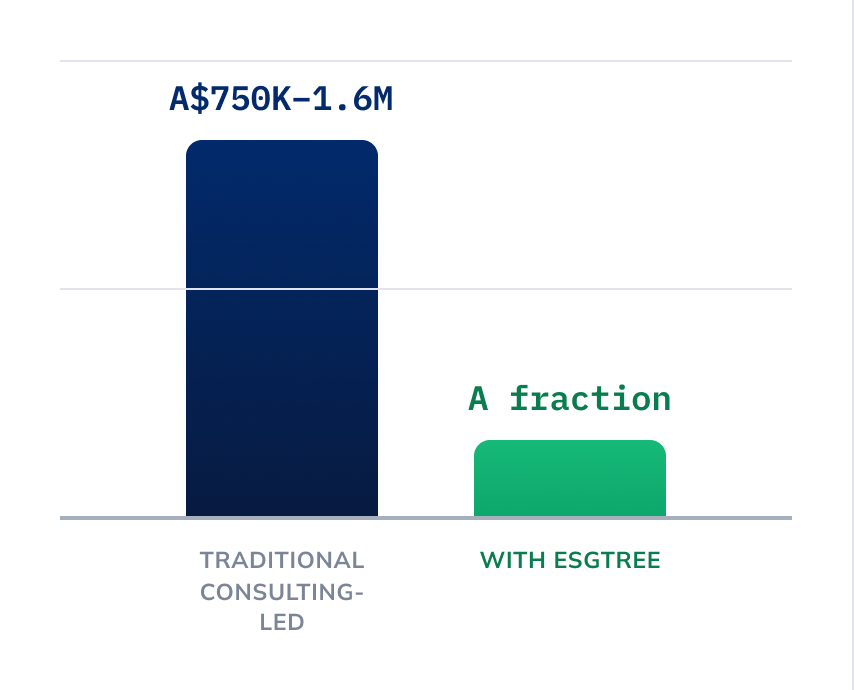

You have a lean sustainability team

Run the full AASB S2 process without hiring a large internal team. The platform structures the work and routes data requests straight to the right owners across your business.

You want to avoid rework every year

Build your data structure once. As Scope 3 relief expires and assurance scope widens, the same foundation carries forward, with no rebuilding each reporting cycle.

You want to stay current as rules evolve

NGA Factors update annually and the platform keeps pace with AASB S2 amendments and tightening assurance requirements, so your process stays compliant as the regime matures.

Built for Australia

Scope 1 and 2 calculated with the Australian National Greenhouse Accounts (NGA) Factors, updated annually. Both location-based and market-based Scope 2 methods supported.

Financed emissions

A dedicated module for banks, super funds, and asset managers, aligned to PCAF methodology and the AASB S2025-1 amendments for Scope 3 Category 15 disclosures.

AASB S2 & IFRS S2

Because AASB S2 is substantially equivalent to IFRS S2, the same underlying data supports both. Relevant for entities with parents or investors reporting under IFRS S2 abroad.