The rallying cry of the American Revolution – no taxation without representation – is today taken as self-evident but deserves a re-examination in light of the climate crisis and sustainable…

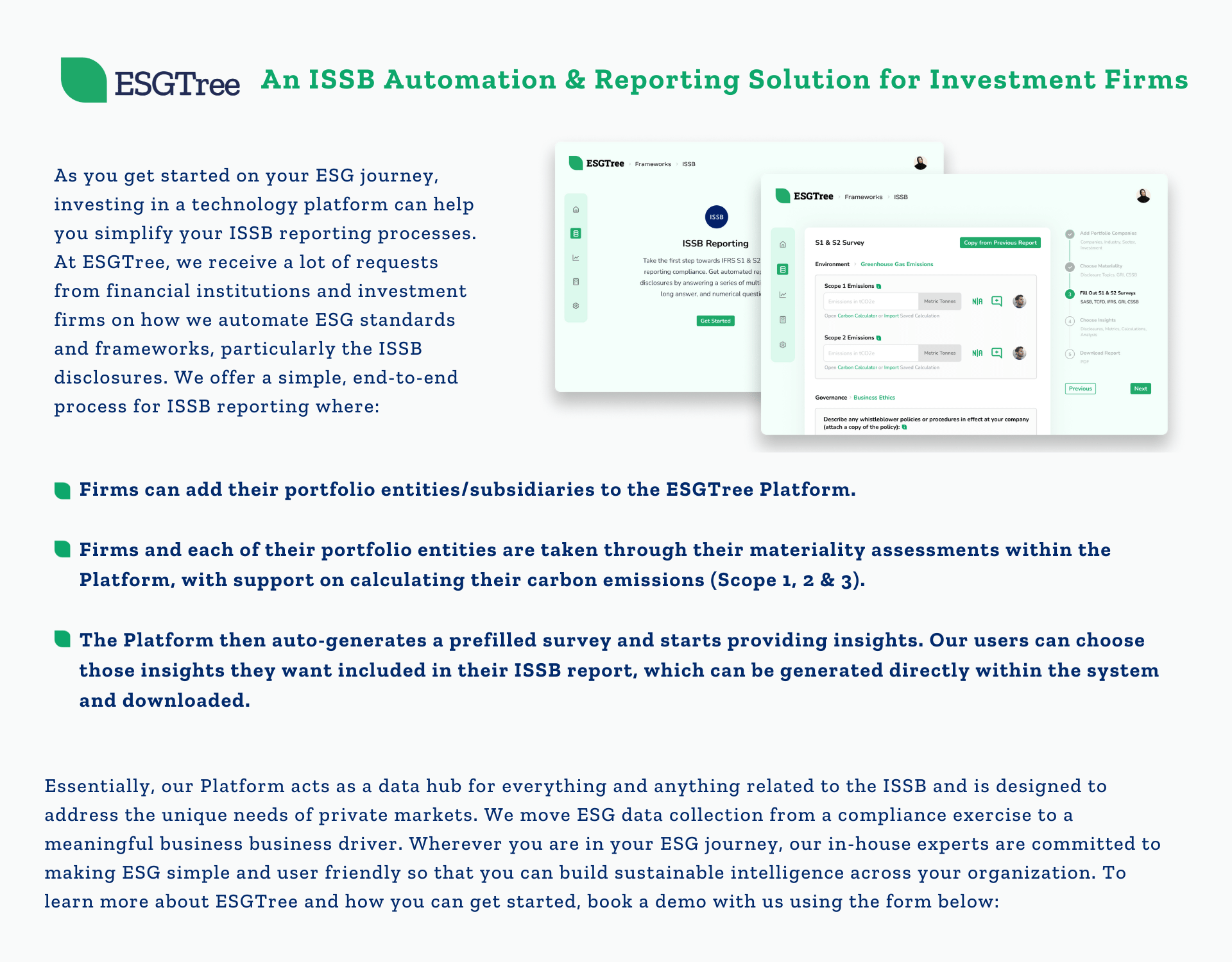

Differences that Make a Difference: What distinguishes ESGTree from its competitors. Over the past four years, one of the most common questions we get is: What differentiates ESGTree from

The rallying cry of the American Revolution – no taxation without representation – is today taken as self-evident but deserves a re-examination in light of the climate crisis and sustainable…

Last year, private equity firm the Carlyle Group and pension fund the California Public Employees Retirement System (CalPERS) announced what could become a game changer for the private equity industry.…

By market size alone, impact investing might be far smaller than ESG investing, but its unique profile makes it a critical part of sustainable finance. ESG assets are on course…