Why ESGTree? – Differences that Make a Difference

Differences that Make a Difference: What distinguishes ESGTree from its competitors. Over the past four years, one of the most common questions we get is: What differentiates ESGTree from

SFDR Reporting Solution for Financial Institutions

Our fully integrated SFDR Reporting Software addresses these challenges by:1)Translating legislation & technical indicators into an intuitive interface that enables portfolio companies to track & improve their performance.

Podcast: Winning ESG Integration Strategies for GPs

In this insightful episode, our AI-powered hosts, Rich and Rachel Green, dive into the critical strategies General Partners (GPs) can adopt to stay ahead of Limited Partner (LP) DDQs and…

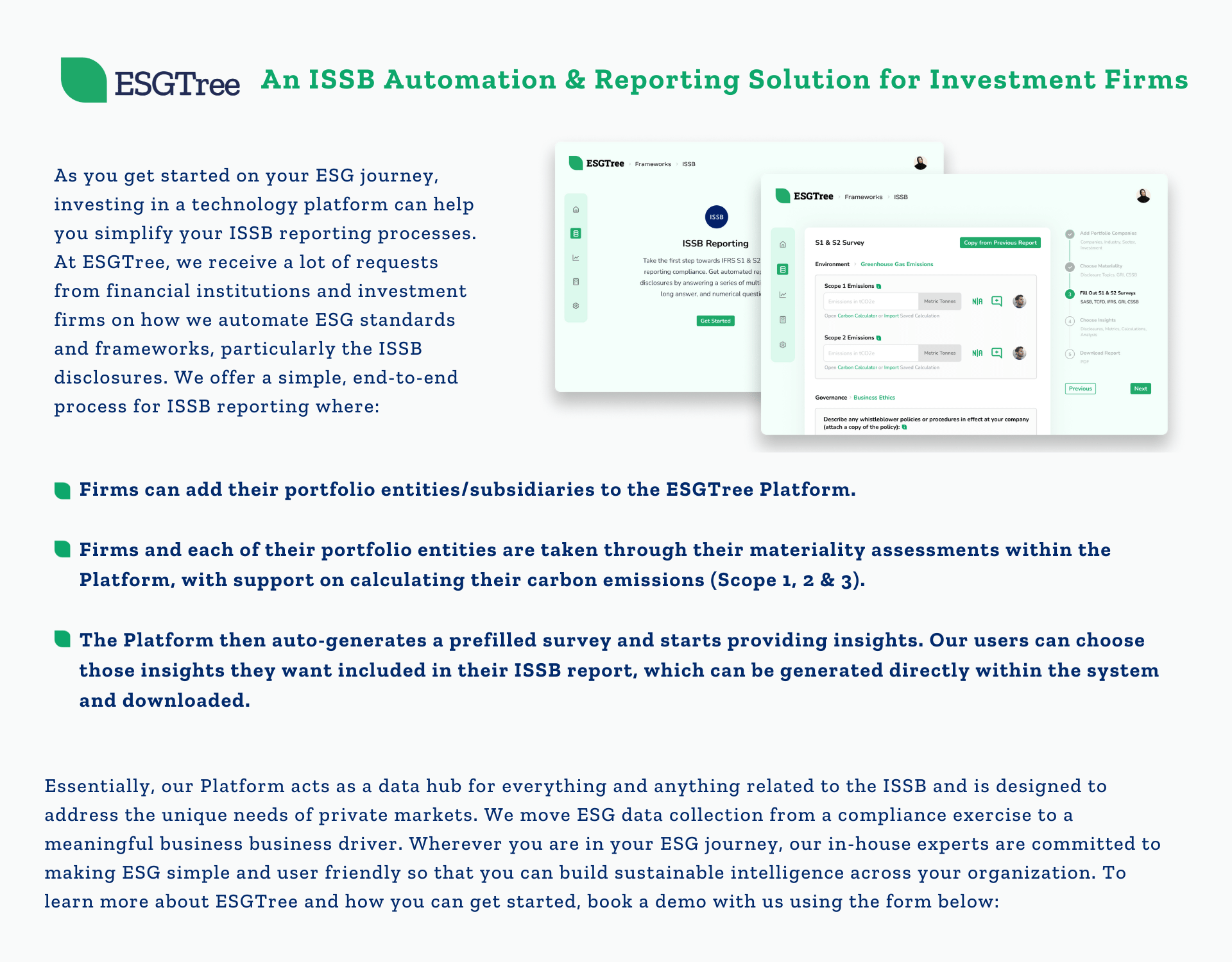

Guiding Financial Institutions on the Path to Net Zero

ESGTree is a cloud-based Environment, Social and Governance (ESG) data management and reporting platform for financial institutions. Our Carbon Calculator and automated climate reporting software are just some of the…

Financed Emissions Unlocked: Strategic Insights for LPs and Pension Funds

In this insightful episode, our AI-powered hosts, Rich and Rachel Green, dive into the critical strategies General Partners (GPs) can adopt to stay ahead of Limited Partner (LP) DDQs and…